It’s Not About Paying Less Tax. It’s About Not Paying More Than You Should

Late evening. End of financial year.

You’re looking at your numbers. Revenue looks fine. Expenses are there. Everything seems… reasonable.

Then the tax estimate shows up.

Higher than expected.

You pause. Not because you didn’t plan for taxes.

But because something feels off.

You didn’t do anything wrong.

But you’re not sure if you did everything right either.

That difference matters.

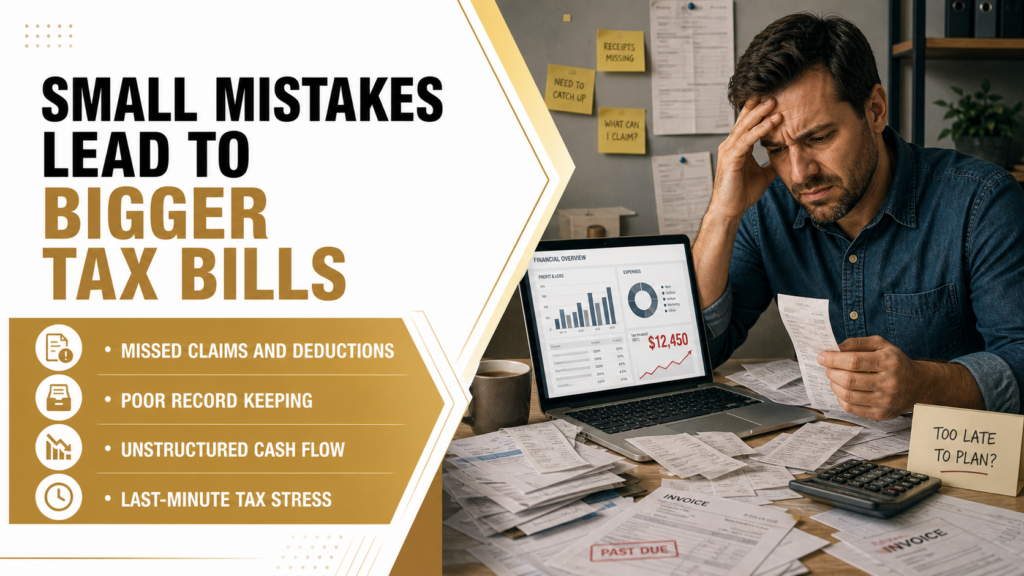

Most small businesses don’t overpay taxes due to big mistakes.

They overpay because of small things that go unnoticed all year.

That’s where the best accountant for small businesses makes a real difference.

Where Money Quietly Slips Away

Tax doesn’t suddenly become expensive at the end of the year. It builds up through small decisions made over time.

- Expenses not recorded properly

- Deductions missed or misunderstood

- Income not timed efficiently

- Cash flow not aligned with tax obligations

Individually, these seem minor.

Together, they increase your tax bill.

Not dramatically. But consistently.

The Difference Between Filing Taxes and Planning Taxes

Most businesses think of accounting as something that happens after the year ends. Prepare reports. File returns. Done. That’s compliance. But real savings come from something else. Tax planning for small businesses in NZ happens during the year.

It’s about:

- Knowing what to claim and when

- Structuring income in smarter ways

- Managing expenses with intention

- Adjusting before deadlines, not after

By the time the year ends, most tax outcomes are already decided.

A good accountant works before that point.

Small Business Tax Deductions New Zealand Businesses Often Miss

This is where things get practical. Not all deductions are obvious. And not all are used correctly.

Some common areas where businesses lose money:

- Home office expenses that are under-claimed

- Vehicle usage not tracked properly

- Software and subscriptions missed

- Professional services not categorised correctly

- Asset purchases not timed strategically

The issue is not a lack of awareness. It’s a lack of structure. When records are inconsistent, deductions become harder to justify. And when they’re not claimed properly, they’re effectively lost.

Provisional Tax: Small Business Owners Struggle With

Provisional tax is one of the biggest stress points.

- Not because it’s complex.

- But it affects cash flow directly.

Many business owners either:

- Underestimate and face penalties

- Overestimate and restrict cash unnecessarily

A well-managed, provisional tax New Zealand small business strategy balances both.

It aligns payments with actual performance, not guesswork.

This is where planning saves money.

- Not by reducing the tax itself.

- But by avoiding penalties and preserving cash flow.

The Cost Question Everyone Asks

“How much does an accountant cost for a small business in NZ?”

It’s a fair question.

But it’s often looked at in isolation.

The better question is:

“What is the cost of not having the right accountant?”

Consider this:

| Scenario | Outcome |

| DIY or minimal support | Missed deductions, higher tax |

| Reactive accountant | Compliance met, limited savings |

| Proactive accountant | Structured planning, optimised tax position |

The difference is not always visible immediately.

But over time, it compounds.

Common Tax Mistakes Small Business Owners in New Zealand Make

Most tax issues are not dramatic.

They are routine habits that go unchecked.

- Mixing personal and business expenses

- Leaving bookkeeping until the last minute

- Claiming deductions without proper documentation

- Ignoring small inconsistencies in reports

- Not reviewing financials regularly

These don’t always trigger immediate problems. But they reduce accuracy. And when accuracy drops, tax efficiency follows.

What a Great Accountant Actually Does Differently

It’s not just about knowledge. It’s about timing, structure, and attention.

A strong accountant:

- Reviews your numbers regularly, not just annually

- Flags issues before they become costly

- Helps you understand your financial position

- Aligns your decisions with tax outcomes

- Keeps your records clean and consistent

This is not about doing more work. It’s about doing the right work, earlier.

A Shift in Perspective

Think about your last financial year. Not just the results. The process.

- Did you feel in control of your numbers?

- Did you understand your tax position clearly?

- Did you make decisions based on data or instinct?

If the answer is uncertain, there’s room for improvement.

And that improvement usually comes from better financial guidance.

A More Practical Way Forward

Working with a firm like Elite Accounting Limited- Chartered Accountants shifts accounting from a once-a-year task to an ongoing process of clarity and control.

It means:

Your records stay accurate throughout the year

Your deductions are captured consistently

Your tax position is understood before deadlines

Your decisions are guided by real financial insight

That’s where the real difference lies.

Not in last-minute adjustments.

But in steady, informed financial management that keeps your business efficient, compliant, and in control.

FAQs

Yes, through proper planning, accurate deductions, and better financial structuring.

Home office, vehicle use, subscriptions, and small operational expenses.

No, but it can be managed more accurately to reduce stress and penalties.

Regularly. Not just at year-end.

In most cases, yes. The value often exceeds the cost through better tax outcomes.

Final Thought

Tax time doesn’t create problems. It reveals them.

If your records are clear, your planning is structured, and your decisions are aligned, tax becomes predictable.

If not, it becomes expensive.